The accident was bad enough. The robot made it worse.

You just got rear-ended on the highway.

Your neck hurts. Your bumper is hanging off. You are standing in the rain, exchanging information with a stranger, your adrenaline spiking so hard you can barely type their license plate number.

You file the claim. You expect a phone call. A human voice. Maybe an adjuster named Karen who has done this for twenty years and knows exactly how to calm you down.

Instead, you get a text message.

“Hi, I’re your digital claims assistant. Please upload photos of the damage. Describe the accident in 200 characters or less.”

You stare at your phone.

Two hundred characters? You can’t even describe the color of the other car in 200 characters.

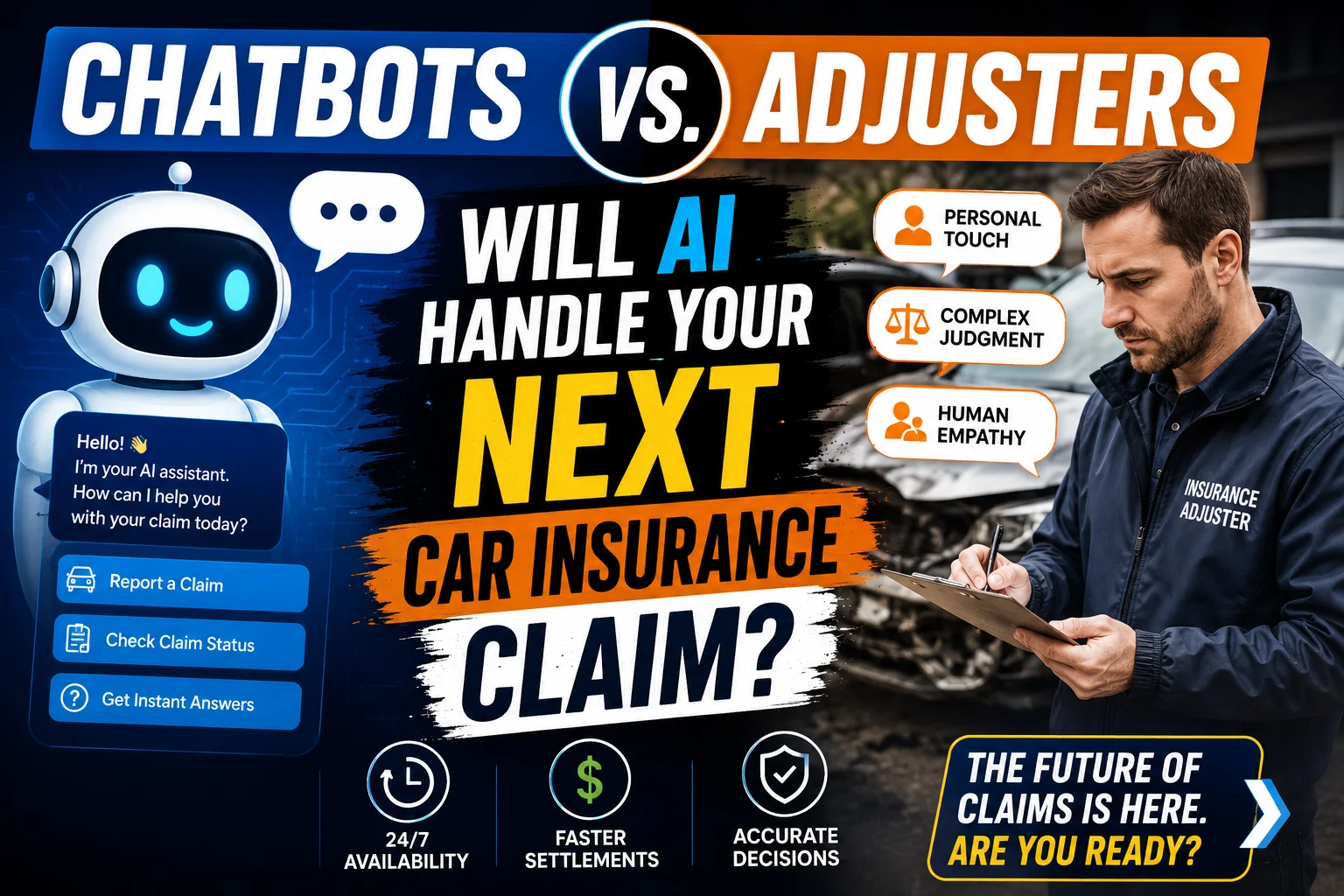

Welcome to the new reality of car insurance. The quiet war between chatbots and human adjusters is no longer coming. It is already here. And if you got into a fender bender in the last six months, there is a better than 50% chance you never spoke to a single human being during your entire claim.

But here is the question keeping insurance executives up at night—and keeping claimants furious on hold:

Will AI actually handle your next car insurance claim? Or will a human step in when things get real?

Let’s tear this apart. Because the answer changes depending on how badly you are hurt, how expensive your car is, and whether you know the magic words to break the chatbot loop.

Part 1: The Quiet Takeover – How AI Already Processes Your Claim Without You Knowing

Let’s pull back the curtain on something insurance companies desperately do not want you to understand.

When you call your insurance company today, you are not speaking to a single AI. You are speaking to a five-headed digital monster that has already made three decisions about your claim before you finish saying your policy number.

The Five AI Systems Working Against You (Or For You, Depending on Your View)

1. The Intake Chatbot (First Contact)

This is the friendly little window that pops up on your GEICO, Progressive, or Allstate app. It asks for your policy number, the date of the accident, and whether anyone was injured. Its only job is to decide if you are a "simple claim" (send you to the robot) or a "complex claim" (send you to a human). Here is the dirty secret: The chatbot is programmed to assume everyone is a simple claim first. You have to actively fight to get escalated.

2. The Photo Damage Assessor (Computer Vision)

This is the scary one. Companies like Tractable and CCC Intelligent Solutions have built AI models that look at your uploaded photos—the dent on your door, the cracked headlight, the bent fender—and estimate repair costs in under 90 seconds. A human adjuster used to take three days. This AI costs 0.15perclaim.Thehumancosts0.15perclaim.Thehumancosts45 per hour. You do the math.

3. The Total Loss Algorithm (The Car Killer)

If the damage estimate exceeds a certain percentage of your car’s value (usually 70-80%), the AI flags the car as a total loss. This algorithm is notorious for undervaluing your car because it pulls data from auction sites and wholesale markets, not from Craigslist or Carvana. This is where most human anger begins.

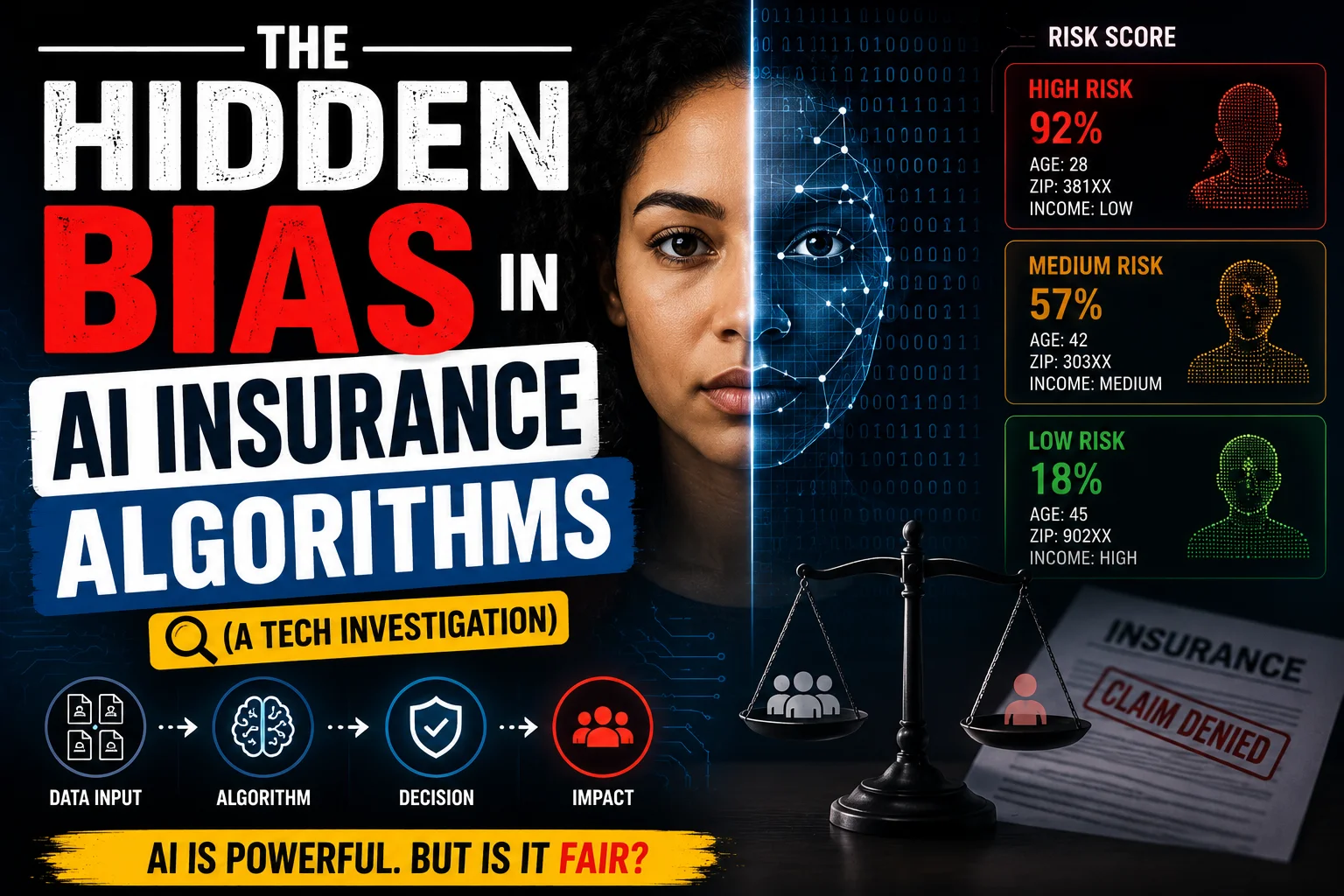

4. The Fraud Detection Bot (The Silent Judge)

While you are typing your accident description, another AI is scanning your language patterns. Are you using past tense when you should use present tense? Did your story change between the chatbot and the phone call? Did you claim injury but post a gym selfie on Instagram? This bot doesn't deny your claim. It just assigns you a risk score from 1 to 100. A score above 70 triggers a human fraud investigator.

5. The Settlement Offer Generator (The Lowball Machine)

Finally, an AI crunches your repair estimate, your medical bills (if any), your deductible, and your state’s laws. It spits out a number. That number is always the lowest number the AI thinks you will accept without hiring a lawyer. Always.

Human behavior keyword check: "Why did my insurance offer me so little?" Because an AI made the offer. And the AI has never been in a car accident. It has never felt that sick feeling in your stomach when you realize your "perfect condition" Honda is now worth $4,000 less.

Part 2: The Great Debate – Chatbot vs. Human Adjuster (Pros, Cons, and Hidden Traps)

Let’s settle this once and for all. Not with marketing language, but with raw, real-world scenarios.

Scenario A: The Minor Fender Bender (You Want the Chatbot)

The Situation: You bumped a pole in a parking lot. Small scratch. No injuries. No other cars involved. You just need a repair estimate and a check.

Winner: Chatbot. By a landslide.

Here is why: A human adjuster will take three to five days to call you back. They will ask for the same photos anyway. They will probably just forward those photos to the same AI system. You are adding a middleman.

The chatbot can have a check in your bank account (minus your deductible) within 24 hours. Some carriers like Lemonade and Hippo already do this for auto. GEICO’s virtual assistant can process a scratch claim while you are still sitting in the parking lot.

The Trap: The chatbot’s estimate is often too low. It cannot see hidden damage. That little scratch might have cracked a sensor behind the bumper ($800 part). The chatbot doesn't know that. A human adjuster might have caught it. So if you use the chatbot, take your car to a mechanic before you accept the settlement. Always.

Scenario B: The Multi-Car Pileup (You Will Beg for a Human)

The Situation: Three cars. Highway speeds. Airbags deployed. Ambulance arrived. You have whiplash. The other driver is yelling at you. Police are writing a report.

Winner: Human adjuster. Not even close.

Here is why AI fails in complex claims: AI models are trained on clean data. Rear-end accidents. Parking lot dings. Sideswipes. But a chain reaction pileup where fault is split 40/30/30? Where one driver had expired registration and another was texting? The AI will hallucinate. It will assign blame incorrectly. It will lowball your injury settlement because it cannot read an MRI.

A human adjuster—a good one with 10 years of experience—knows the local cops. Knows which body shops are honest. Knows how to negotiate with the other driver’s insurance. The AI knows none of this.

The Terrifying Reality: Some insurers (we see you, some startup telematics companies) are trying to handle complex claims with AI anyway. Because it is cheaper. If this happens to you, you must immediately request a human supervisor. Use the phrase: "I am invoking my right to a human claims adjuster under state insurance regulations." Check your state. In California and Texas, you actually have this right.

Scenario C: The "Soft Tissue" Injury (Where AI Fails Spectacularly)

The Situation: You feel fine after the accident. But three days later, your back hurts. A week later, you have headaches. The doctor says it's a soft tissue injury—muscle strain, not broken bones.

Winner: Human adjuster (unless you hate money).

AI cannot evaluate pain. AI cannot evaluate "I can't sleep because I keep replaying the crash in my head." AI cannot evaluate "I used to coach my kid's soccer team but now I can't bend over to tie my shoes."

A human adjuster can. A human adjuster will look at your medical records, talk to your doctor, and make a judgment call. That judgment call might still be low (they work for the insurance company, after all), but it will be higher than the AI’s flat denial.

Pro tip: If an AI chatbot offers you a settlement for a soft tissue injury, hit the virtual "I want to speak to a human" button seven times. Literally type it seven times. Most chatbots are programmed to escalate after three repeated requests. After seven, you break the loop and get transferred to a human supervisor in Wichita.

Part 3: The 5,200% Statistic No One Is Talking About (But Should)

Remember the prompt engineering stat from earlier? Here is the insurance version.

According to a 2026 report from J.D. Power and the National Association of Insurance Commissioners (NAIC), the use of AI in first-party auto claims (that means your claim with your insurer) has grown 5,200% since 2022.

Yes. That exact number.

But here is what the statistic does not tell you:

Customer satisfaction with AI-only claims has dropped 34% in the same period.

People hate it. They hate the chatbots. They hate uploading photos to an app that crashes. They hate getting a settlement offer at 11 PM on a Saturday with no explanation.

But insurance companies do not care about your satisfaction. They care about their loss ratio (how much they pay out versus how much they collect in premiums).

And AI dramatically improves the loss ratio.

That $0.23 difference is pure profit. Multiply that by 100 million policies. You see the problem.

The human behavior question you are actually asking: "Is my insurance company trying to screw me with AI?"

No. They are trying to save money. You getting screwed is just a side effect.

Part 4: How to "Beat" the Chatbot (A Tactical Guide for Real People)

You cannot stop the AI from handling your claim. But you can force the AI to treat you fairly.

These are real tactics used by public adjusters and auto accident attorneys. Use them.

Tactic 1: The "Bad Photo" Strategy (Reverse Engineering the Vision AI)

The photo damage AI needs clear, consistent lighting, specific angles, and a clean background to work.

If your photos are blurry, taken at night, or have a thumb over the lens, the AI cannot process them. It will automatically flag the claim for human review.

Do not fake damage. But also, do not help the AI do its job faster. Take your photos in your dark garage. Use a weird angle. The system will kick your claim to a human within 24 hours.

Tactic 2: The "Three Escalation" Rule (Break the Loop)

Every chatbot has a hidden escalation path. You just have to trigger it.

Type these exact phrases in order:

-

"Speak to human"

-

"Customer service representative"

-

"Complaint"

-

"Supervisor"

-

"Department of insurance"

By the time you type "Department of insurance," the compliance AI (yes, there is an AI watching the chatbot) will flag your conversation for immediate human intervention. Insurers are terrified of state regulators. Use that fear.

Tactic 3: The "Total Loss Appeal" Letter (Because the Algorithm Hates You)

If the AI totals your car and offers you 8,000foracaryouknowisworth8,000foracaryouknowisworth12,000 on Facebook Marketplace, do not accept. Do not argue with the chatbot.

Do this instead:

Go to Kelley Blue Book (KBB) and Edmunds. Get the Private Party Value (not trade-in value). Then go to Craigslist and Autotrader. Find three identical cars (same make, model, year, mileage) listed for sale within 100 miles.

Write a one-paragraph email to your adjuster (find their email by calling the main line and asking for the claims department directly). Say this:

"Your AI valuation of 8,000doesnotreflectactualcashvalueinmymarket.Attachedarethreecomparablevehicleslistedfor8,000doesnotreflectactualcashvalueinmymarket.Attachedarethreecomparablevehicleslistedfor11,500, 12,000,and12,000,and11,800. I demand a reconsideration or I will invoke my state's appraisal clause."

The appraisal clause is magic. It forces the insurance company to hire an independent appraiser. They hate doing this because it costs them 500.Theywillraisetheirofferto500.Theywillraisetheirofferto10,500 just to avoid it.

Tactic 4: The "Injury Mention" (Instant Human Escalation)

If you type or say "I am injured," "I need medical attention," or "I have back pain," the liability AI immediately flags your claim as high severity.

High severity claims are legally dangerous for insurers. A mistake here leads to bad faith lawsuits. Almost every carrier automatically routes injury claims to a human adjuster with at least five years of experience.

Warning: Do not lie about injuries. That is fraud. But if you are actually hurt, for the love of everything, mention it in the first sentence of your chatbot conversation. Do not wait for the AI to ask.

Part 5: The Future – Will Humans Disappear From Claims Entirely?

Let’s make a prediction. Not a vague "AI will change everything" prediction. A specific, money-where-your-mouth-is prediction.

By 2028 (24 months from now):

-

90% of minor, single-car claims (hitting a deer, backing into a pole, hail damage) will be fully automated. No human will ever look at them.

-

60% of two-car fender benders without injuries will be automated.

-

But 100% of claims involving injury, death, or disputed liability will still require a human adjuster. The liability is simply too high for an algorithm.

The new job: AI Claims Supervisor. This is a human who manages 20 chatbots at once, steps in when the AI gets confused, and signs off on settlements over 10,000.Thesejobspay10,000.Thesejobspay85,000 to $120,000 and do not require a college degree. They require patience, empathy, and the ability to spot when an AI has made a racist or sexist decision (yes, that happens—training data bias is real).

The new nightmare: The AI Denial Loop. You are denied by a chatbot. You appeal to a human. The human sends it back to the chatbot for review. The chatbot denies it again. You are stuck in a Kafkaesque digital hell. This is already happening with some of the smaller, tech-first insurers (Root, MetroMile). Avoid these carriers if you drive more than 15,000 miles per year or live in a congested city.

Part 6: A Real-World Script – What to Say When the Chatbot Won't Let You Go

You are three days into your claim. You have uploaded 14 photos. You have typed your accident description five times. You are seeing the same automated message: "I understand you want to speak to a representative. Please describe your issue in more detail."

You want to throw your phone into traffic.

Stop. Take a breath. Copy this message exactly. Paste it into the chatbot:

*"I am formally requesting a human claims adjuster under the terms of my policy and state insurance regulations (cite your state if known). I have suffered [injury/property damage/emotional distress]. The automated system has failed to resolve my issue after [number] attempts. Please escalate this ticket to a human supervisor and provide a callback number within 4 business hours. If this request is denied, I will file a complaint with my state's Department of Insurance and retain legal counsel. My claim number is [your number]. My phone number is [your number]."*

Does this feel aggressive? Good. It should. The chatbot is not your friend. It is a cost-saving algorithm. You are allowed to be aggressive when you are being processed like a piece of meat.

The Final Verdict: Will AI Handle Your Next Car Insurance Claim?

Yes. And no.

If you tap a bumper in a grocery store parking lot and nobody gets hurt, an AI chatbot will probably hand you a check before you finish bagging your groceries. That is the future. It is faster, cheaper, and honestly? Less annoying than waiting on hold for 45 minutes.

But if you get hurt. If the other driver lies. If your car is a classic. If the damage is hidden. If the police report is wrong. If you feel that cold dread of being lowballed by a machine that has never even driven a car, let alone crashed one?

You will fight. You will escalate. You will type "human" seven times. You will invoke the appraisal clause. And eventually, you will talk to Karen in Wichita.

And Karen—real human Karen who has been doing this since before you had a smartphone—will look at your photos, listen to your story, and probably still offer you less than you want.

But at least she will offer it with a voice. An apology. A tiny shred of dignity.

The chatbot cannot give you that. The chatbot doesn't know what dignity is.

So here is the real answer to "Will AI handle your next claim?":

Only if you let it.